When did New Zealanders start pinning their retirement hopes on a big tax-free capital gain? Analysis by Max Rashbrookes suggests one driver was the decline of corporate pensions during the pro-market revolution of the 1980s.

A few years ago I wrote a column arguing that, over a generation, house prices in New Zealand needed to fall 40% if they were to become once more affordable. This was, it’s fair to say, controversial: the online response was heated, even at times furious.

One commenter claimed I was advocating for a “handout” from existing homeowners to prospective ones, suggesting he had so strongly internalised the idea of his home’s current value being an actual property right that – in his mind – any decrease in it was like giving his money to others.

Even more intriguingly, someone else wrote that they felt I was attacking the New Zealand “dream” of owning one house to live in and one for retirement income. “Hah,” I thought to myself. “When did that become the New Zealand ‘dream’?” And then I thought: “Hang on – when did that become the New Zealand dream?” Middle-class New Zealanders have long sought to use residential property for current income. But for their retirement?

This has, of course, only ever been a “dream” attainable by a few. For all their dominance of political debate, the number of property investors in 2021 was just 530,000, according to analysis by data firm Valocity. That’s about one in seven adults. But because they are relatively well-off and influential adults, their dreams matter. One of the arguments already advanced against a capital gains tax, for instance, is that it will harm “mum and dad” investors who have pinned their retirement hopes on a big tax-free capital gain. Never mind that these investors, according to Valocity, own just one-third of rental properties, the remainder lying in the hands of large-scale landlords. Such arguments still have rhetorical power.

So I kept puzzling over the conjunction of retirement savings and rental properties. And then someone, at a social gathering, said to me, surely it’s to do with the collapse of corporate pensions. At which point a lightbulb went on. Many New Zealand firms had, pre-1980s, provided relatively generous pensions to their staff; as with the welfare state, the loose assumption was that powerful players with deep pockets – big businesses and big governments – should look after those with lesser means. The world was a difficult and risky place, and there were limits to how well the average person could “insure” themselves against those risks – could protect themselves against economic shocks, in other words – if acting alone.

By the 1970s, the state shouldered the main burden, paying New Zealand Superannuation at a rate designed to keep recipients out of poverty. But, then as now, that was insufficient for a comfortable retirement: hence the importance of the company pension, for the admittedly well-off slice of the population that received one.

All this changed in the pro-market revolution that swept the west in the 1980s. The individual was held responsible for their outcomes in life, and the most efficient way to solve problems – including the puzzle of retirement savings – was for people to make their own private investments in the free market. Risks were shifted onto individuals. Firms felt less responsibility to their staff, and cut back their corporate pensions. Many got out of the game altogether, and the remaining players shifted away from relatively generous “defined benefit” schemes, based on the employee’s final salary and length of service, and towards less generous “defined contribution” schemes, based more on the employees’ own savings.

It made intuitive sense, then, that as corporate pensions declined, their former recipients started searching for another source of retirement income, and looked to real estate as their saviour. But did the data back this up?

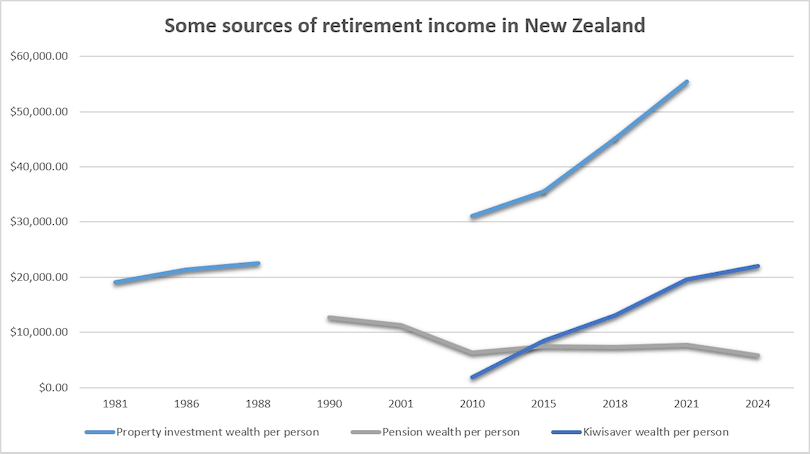

The answer, according to the data I’ve compiled, is a tentative yes. Immediately obvious is the decline in the average value of private pension wealth from 1990 onwards, and the even greater increase in property investment wealth. (In both cases, the total dollar value invested in each category has been divided by the New Zealand population, and adjusted for inflation.) From 2008 onwards, Kiwisaver emerges as a third source of retirement income; a classic “Third Way” policy, it is both individualistic and communitarian, relying essentially on the individual’s contributions but bolstered by state top-ups.

Caveats to this analysis abound, however. Correlation is famously not causation: corporate pensions might have declined, and property investment risen, for unrelated reasons. The housing market has been radically changed since the 1980s, in ways that have nothing to do with retirement per se: think about the decline in house-building volumes, the sale of state housing, the more general retreat of the state from subsidising first homes and mortgages, the creation of tax advantages for property investment, and the much wider trend for the “financialisation” of housing. We have no way of knowing how much investment property has a specific retirement focus.

The data assembled here are also seriously partial, pieced together from multiple different surveys and laced with all kinds of gaps and assumptions. (Individuals’ entitlement to New Zealand Superannuation could, for instance, be rolled into an estimated lump sum, and charted as another form of “wealth”.) This should be seen as a first, rapid pass at answering a crucial question, rather than a definitive answer.

Even if the data could be corroborated, a further puzzle presents itself. Why, if middling and well-off New Zealanders wanted another source of retirement income, did they turn to rental property and not, say, the stockmarket? The tax advantages for housing offer one simple answer. Another is located in this country’s appallingly low levels of financial literacy. Housing is easy to understand; financial investments seem complex and scary.

There is also a justifiable sense that non-housing investments are not as well-regulated as they might be. All financial sectors experience occasional crises, but New Zealand’s are especially severe: our 1987 stockmarket crash was a particularly brutal version of the type, and throughout the 2000s our regulators were having a pleasant snooze while finance companies engaged in the risk-taking behaviour that eventually saw them collapse en masse, taking $3bn in people’s savings with them.

In this light, property investment looks a far safer bet. So if the country is to end its over-investment in housing, build up its export sector – and, potentially, introduce a capital gains tax – it may need to provide alternative retirement options, whether that means leaning more heavily on Kiwisaver, or something else. And that, in turn, may require steps to make financial investment safer. One of the most unexpected roots of the housing crisis, in short, may be our failures in financial regulation.